Credit can be a scary thing. Reports indicate that around 30% of scorable people in the US have a credit score below 600.

This just won’t do. Today, we need credit for almost everything. I am not saying that you should live beyond your means, in fact, you must be careful NOT to since it is almost impossible to have good credit when you spend more than you earn. The fact remains though, it is increasingly harder to do simple things like rent a car, get a good insurance rate and rent an apartment or home without a decent credit rating, and forget owning a home if you don’t get that score up.

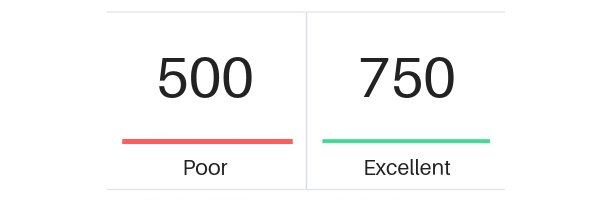

Here are a few things I did when I decided to work on my poor credit. I started in December of last year, with a score of under 500, and this month, I hit the 750 mark.

In the past I had two cars repossessed, and a score of credit card chargeoffs and derogatory marks. Some were currently affecting my credit, some were long gone, but the point I am trying to make is that I was starting over after having screwed the pooch pretty badly in the past. More than once.

If I could bring my score up into the excellent range in one year, you can fix your credit as well.

DISCLAIMER: I want to note here, I am no financial expert, I do not work as any sort of financial professional, and I was not paid or otherwise compensated in any way for any of the information in this post. This is all based on my own personal experience, and what I did to improve my own situation, and should not be taken as professional advice in any way.

- Utilize a service like Credit Karma. There are a few out there. Some charge a membership fee, others don’t. Credit Karma is totally free, and you can check your accounts and scores from two agencies as much as you want, with no damage to your score, and no hidden charges. Use your chosen service to see what is currently on your report, make sure everything is accurate, and take steps to pay off your debts, or dispute anything that isn’t right. After you have taken care of the preliminaries, you can keep using this service to track your progress. I look at mine weekly, and it gives me a breakdown of everything. My balances, my payment history, and lets me know if anyone has looked at my credit lately so I can make sure no one is using my credit but me.

- Build credit with a secured Credit Card. There are many out there to choose from. I personally went with my bank’s secured Mastercard, as I wasn’t required to put the full credit line down as a security deposit, they gave me a $500 credit line in exchange for a $99 deposit. After a year of on-time payments, the status of the card was switched from secured to unsecured, the deposit refunded, and the credit line increased from $500 to $2500.

- Open a few accounts and use them. After I used my secured card for a bit, I opened up two more cards. These were unsecured with low balances. I used them, made a few minimum payments, then paid them off to avoid lots of interest. Your credit score improves the more accounts you have open and current. A good way to boost your score is to have several open accounts while keeping your usage at around 30% or lower. A good way to do this is to set up a bill that you pay every month to one card. Each month when that bill auto pays, wait for it to show up on your card statement, and pay it off. Another way is to use one of your cards for the things you buy every day, like gas, coffee, etc. Then when you get your bill every month, pay it in full. As long as your cards are being used and not maxed out, your credit score will continue to rise.

- The final step when you have gotten your credit up to where you want it is to take stock of the accounts you have. Do you have any with super high annual fees or crazy interest rates that are geared towards people building credit? Apply for a better card with no fees and a higher limit and some cashback rewards. If your score is now in the 700s you should have no problem getting accepted for one of these. Once you get it, pay off the starter card, and if the annual fee is high, close it, if it is low, or doesn’t have a fee, keep it open, but don’t use it, and start using the card that has the lower interest rate, and higher credit line. Use it the same way you used your starter cards.

- This is also the time to start thinking about opening a couple different types of credit accounts. If you have a variety of different credit types that you are using responsibly, it reflects positively on your credit report. Examples of different types of credit accounts are installment loans (these include, auto loans, furniture loans, and student loans), mortgages, and credit cards. Once you have your credit in shape, it may be a good plan to open a new type of credit account so you can show diversity to future lenders.

These tips will help you to build and maintain a steady good score and enable you to use your good credit whenever life hands you a situation where you need it. To buy that home you have had your eyes on, or to upgrade your vehicle, or to get that loan you want to refurbish your bathroom. Maybe that dream vacation isn’t so out of reach now that you have a little more financial freedom. However you decide to use your credit, the fact remains that it is a necessity of the modern adult, and it may not be as hard as you may think to get yours into shape.

Thanks for reading!

One thought on “How I Went From Poor to Excellent Credit in 12 Months”